Written Commentary

Price Overview

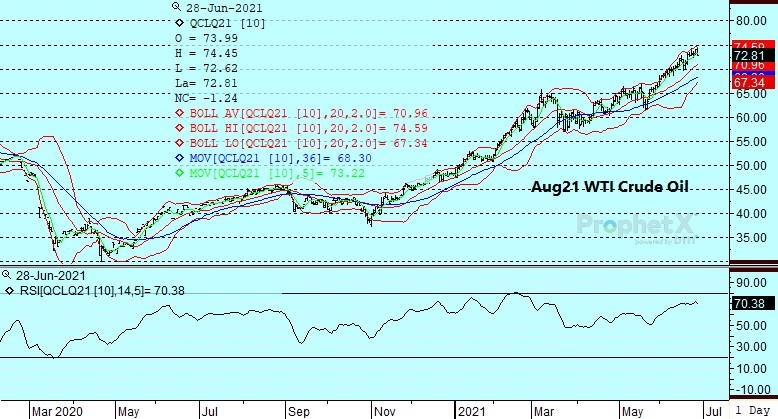

The petroleum complex failed to follow-through on early strength and came under concerted selling pressure as values staged a key reversal following a move to new highs for the move basis Aug WTI crude. Early strength linked to the prospects for growing tightness in inventory levels as we move through the summer and discipline by OPEC with respect to tapering of production curbs; gave way to selling linked to surging COVID-19 infections in Europe and Asia as the Delta variant spreads with some countries such as Australia bringing back lock-downs. The increase in lock-downs in some areas has fostered some fear that the recovery in demand as the summer progresses might be overestimated. The resumption of talks between Iran also was in the background although it is unclear on how quickly any removal of sanction s will take place given the US attacks against Iranian backed militias in Syria and Iraq this weekend and on uncertainty linked to whether Iran will extend a UN monitoring deal which lapsed last week.

The market will be focused on the OPEC + meeting which takes place Thursday and whether additional increases in output are warranted. Reports that Russian output levels did not increase might make it easier to come to a consensus on how quickly output increases might be pursued. Currently most analysts expect a production increase of 500 tb/d for August but more important will be how quickly they are prepared to increase production if current deficit forecasts for the 4th quarter of near 2 mb/d are maintained. In the background, remains the lack of strong increases in shale production in the US to counter the disciplined approach so far of OPEC in raising production levels. We suspect that the prospect of a US infrastructure package will support values on pullbacks but the pickup in COVID lock-downs globally might remain a source of uncertainty and be a destabilizing influence on values in the near term until a clearer demand picture evolves. In addition, the prospective sale of up to 80 mb of crude from the SPR also might pose some modest resistance psychologically as well.

The need for OPEC to expand output as non-OPEC producers appear unable to quickly ramp up output suggests a tightening situation, which will need to be addressed in coming months. So far the discipline OPEC has shown continues to be a surprise given the prevailing price levels. In the absence of any action from the cartel to increase production substantially along with slow progress toward lifting export sanctions on Iran, we believe the market will continue to move toward the 2018 highs near 76.90 in prompt WTI crude as stocks continue to be drawn down throughout the summer. Downside support is likely near the 68.00 level basis August.

Natural Gas

Nat Gas continued the surge higher reaching new highs for the move of 3.653 basis August and reaching levels not seen since January of 2019. Although milder temps are being forecast for the eastern half of the Southern US in the 8-14 day forecast, the record heat in the North West where temperatures have topped 100 degrees for the third day in a row and are forecast to reach up to 109 degrees today in Seattle compared to normal temps of 76 degrees has raised concerns over the adequacy of hydro power supplies in the Northwest.

Near term the market might revert back to the somewhat cooler conditions in the US in mid July. Demand for LNG cargoes has remained high from overseas but export levels have slipped somewhat due to short term maintenance at Gulf Coast facilities. US pipeline exports to Mexico are maintaining record levels in June A slightly cooler situation next week and expectations for a build in Nat Gas inventories of 76 bcf compared to 55 bcf last week should provide some modest resistance near term toward the 3.70 area Aug particularly given the expiration of the July Nat Gas today with support likely on pullbacks into the 3.35-3.40 area.

Charts Courtesy of DTN Prophet X, EIA, Reuters

The authors of this piece do currently maintain positions in the commodities mentioned within this report.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.